When filling out a Business Credit Application form, it's essential to approach the process with care. Here are some key dos and don'ts to keep in mind:

The Business Credit Application form shares similarities with the Personal Credit Application form. Both documents require detailed information about the applicant’s financial history, including income, debts, and credit scores. While the Business Credit Application focuses on the financial health of a business, the Personal Credit Application centers on individual creditworthiness. Each form aims to assess the risk involved in extending credit, ensuring that the lender has a comprehensive understanding of the applicant's financial situation.

Another document that resembles the Business Credit Application is the Loan Application form. Like the Business Credit Application, the Loan Application seeks to gather essential information about the applicant's financial status. This includes income verification, existing debts, and the purpose of the loan. Both forms are designed to evaluate the applicant's ability to repay the borrowed amount, thus aiding lenders in making informed decisions.

The Supplier Credit Application form is also similar to the Business Credit Application. This document is used by suppliers to assess the creditworthiness of businesses seeking to establish trade credit. It typically requires information about the business’s financials, trade references, and payment history. Both forms serve the purpose of mitigating risk for the supplier or lender by ensuring that the applicant has a reliable track record of managing credit responsibly.

The Commercial Lease Application form shares characteristics with the Business Credit Application as well. This document collects financial and operational details from businesses looking to lease commercial space. Just as the Business Credit Application evaluates the financial stability of a business, the Commercial Lease Application assesses the ability of the business to meet lease obligations. Both forms aim to protect the interests of the party extending credit or leasing property.

The Business Loan Proposal is another document that aligns with the Business Credit Application. This proposal outlines a business’s need for funding and includes financial projections, business plans, and repayment strategies. Similar to the Business Credit Application, it requires a comprehensive overview of the business’s financial health. Both documents are crucial for lenders to understand the potential risks and rewards associated with financing a business.

The Vendor Application form is comparable to the Business Credit Application as well. This form is utilized by vendors to evaluate businesses seeking to establish a credit line for purchasing goods or services. Information about the business’s financial standing and credit history is collected, mirroring the approach taken in the Business Credit Application. Both documents help vendors determine the credit limits they can extend based on the applicant's reliability and financial capability.

For those looking to secure a rental property, completing a well-structured lease document is vital. You can find a comprehensive guide on how to fill out a Lease Agreement form for your rental needs to ensure all terms are clear and legally binding.

The Financial Statement is also similar in purpose to the Business Credit Application. This document provides a snapshot of a business's financial condition, including assets, liabilities, and equity. It is often required alongside the Business Credit Application to give lenders a clearer picture of the applicant’s financial health. Both documents work together to facilitate a thorough assessment of the business's ability to manage credit effectively.

Lastly, the Partnership Agreement can be seen as related to the Business Credit Application. While the Partnership Agreement outlines the terms of collaboration between business partners, it often includes financial obligations and profit-sharing arrangements. Understanding these financial dynamics is crucial for lenders when evaluating a Business Credit Application. Both documents reflect the financial interdependencies within a business structure and the importance of financial transparency in credit assessments.

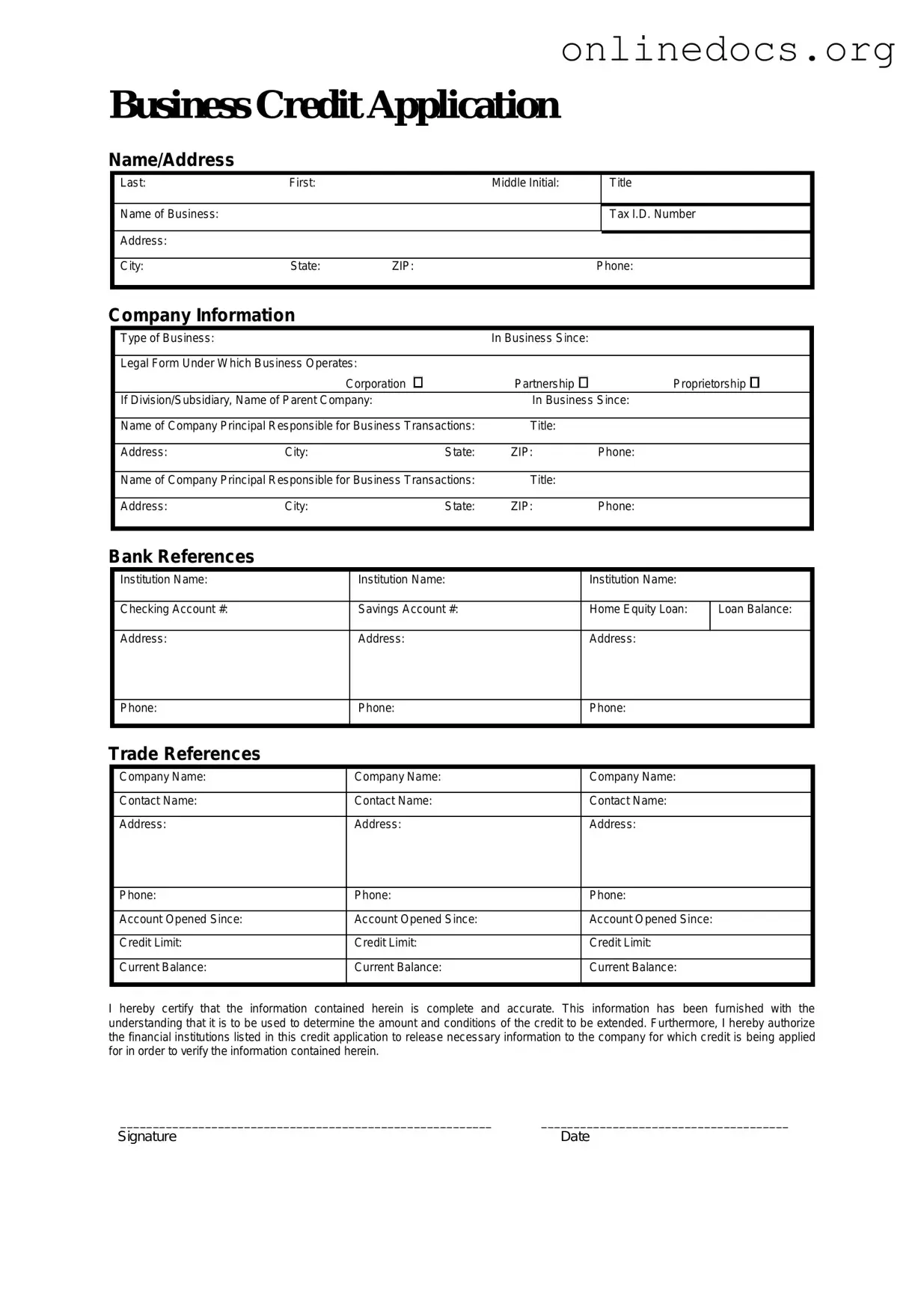

Filling out a Business Credit Application form can be a crucial step for entrepreneurs seeking to secure financing. However, many applicants make common mistakes that can hinder their chances of approval. Understanding these pitfalls can help ensure that your application is both complete and accurate.

One frequent mistake is incomplete information. Many applicants fail to provide all required details, such as business address, ownership structure, or financial information. Omitting even a small piece of information can lead to delays or outright rejection of the application. Always double-check the requirements and ensure that every section is filled out thoroughly.

Another common error is inaccurate financial data. Applicants sometimes provide outdated or incorrect figures. This can misrepresent the financial health of the business and raise red flags for lenders. It’s essential to use the most recent financial statements and ensure that all numbers are accurate before submission.

Some applicants also neglect to review their credit history prior to applying. A poor credit score can significantly impact the decision-making process of lenders. It’s advisable to check your credit report for errors and take steps to improve your score before submitting the application.

Additionally, many people fail to explain the purpose of the credit clearly. Lenders want to understand how you plan to use the funds. Providing a vague or unclear explanation can lead to confusion and may result in a denial. Be specific about your needs and how the credit will benefit your business.

Another mistake involves not including supporting documentation. Many applicants forget to attach necessary documents, such as tax returns, business plans, or financial projections. These documents can provide valuable context and support your application, so make sure to include them when required.

Some individuals also ignore the fine print. It’s crucial to read all terms and conditions associated with the credit application. Overlooking important details can lead to misunderstandings about repayment terms or fees, which could create issues later on. Take the time to understand what you’re agreeing to.

Moreover, applicants sometimes rush the process. In an effort to secure funding quickly, many people fill out the application hastily, leading to mistakes. It’s vital to take your time, review your answers, and ensure everything is accurate before submitting the application.

Finally, a lack of professionalism in communication can also be a mistake. Whether it’s an email or a phone call, maintaining a professional tone is essential. Poor communication can create a negative impression and diminish your chances of approval. Always approach lenders with respect and clarity.

By avoiding these common mistakes, you can enhance your chances of a successful application. Take the time to prepare, review, and present your business in the best light possible. A well-completed Business Credit Application can pave the way for future growth and opportunities.

Roof Certification Form Florida - Anyone seeking to ensure their roof’s reliability should consider obtaining this certification.

To facilitate a smooth rental process, both parties can refer to resources such as the legalformspdf.com for comprehensive templates and guidelines regarding the New York Residential Lease Agreement, ensuring that all essential terms and conditions are clearly defined and agreed upon.

Da Form 31 - Requestors must list their leave address and contact information.

When it comes to the Business Credit Application form, several misconceptions can lead to confusion and missteps. Understanding these misconceptions can help businesses navigate the application process more effectively. Here are eight common misconceptions:

By dispelling these misconceptions, businesses can approach the credit application process with greater confidence and clarity.