When filling out the Florida Promissory Note form, it is important to be mindful of certain practices to ensure accuracy and compliance. Below is a list of things to do and avoid during this process.

The Florida Promissory Note is similar to a Loan Agreement. Both documents outline the terms of borrowing money, including the amount, interest rate, and repayment schedule. A Loan Agreement typically provides more detailed information about the obligations of both the borrower and lender, including consequences for default. However, a Promissory Note is often simpler and focuses primarily on the borrower's promise to repay the loan under specified terms.

Another document that resembles a Promissory Note is a Mortgage. While a Promissory Note represents a borrower's commitment to repay a loan, a Mortgage serves as security for that loan. The Mortgage document gives the lender the right to take possession of the property if the borrower fails to repay the loan. Both documents are essential in real estate transactions but serve different purposes in the lending process.

A Secured Note is also similar to a Promissory Note. Both documents detail the borrower's promise to repay a loan, but a Secured Note includes collateral to back the loan. If the borrower defaults, the lender can claim the collateral to recover the outstanding amount. This added layer of security can make it easier for borrowers to secure loans, as lenders have a tangible asset to protect their investment.

The Florida Promissory Note shares characteristics with an IOU (I Owe You). An IOU is an informal acknowledgment of a debt, indicating that one party owes money to another. While an IOU may lack the formal structure and legal enforceability of a Promissory Note, both documents serve the purpose of recording a debt. However, a Promissory Note typically includes specific terms regarding repayment, making it a more comprehensive and binding document.

A Business Loan Agreement is another document akin to a Promissory Note. This agreement outlines the terms of a loan specifically for business purposes. Like a Promissory Note, it details the loan amount, interest rate, and repayment schedule. However, a Business Loan Agreement often includes additional clauses related to business operations, financial reporting, and other obligations that are specific to the business context.

Understanding the importance of a carefully drafted Release of Liability form is essential for anyone organizing activities that involve risk. This document not only protects the organizer from future claims but also ensures that participants are aware of the potential hazards they may encounter. By utilizing this form, parties can establish a clear understanding of their rights and responsibilities, fostering a safer environment for all involved.

Finally, a Personal Loan Agreement is similar to a Promissory Note in that it establishes the terms of borrowing between individuals. Both documents specify the loan amount, interest rate, and repayment terms. However, a Personal Loan Agreement may also include clauses regarding the relationship between the borrower and lender, which can address issues such as payment flexibility or the consequences of late payments. This document is often used in situations where a personal connection exists between the parties involved.

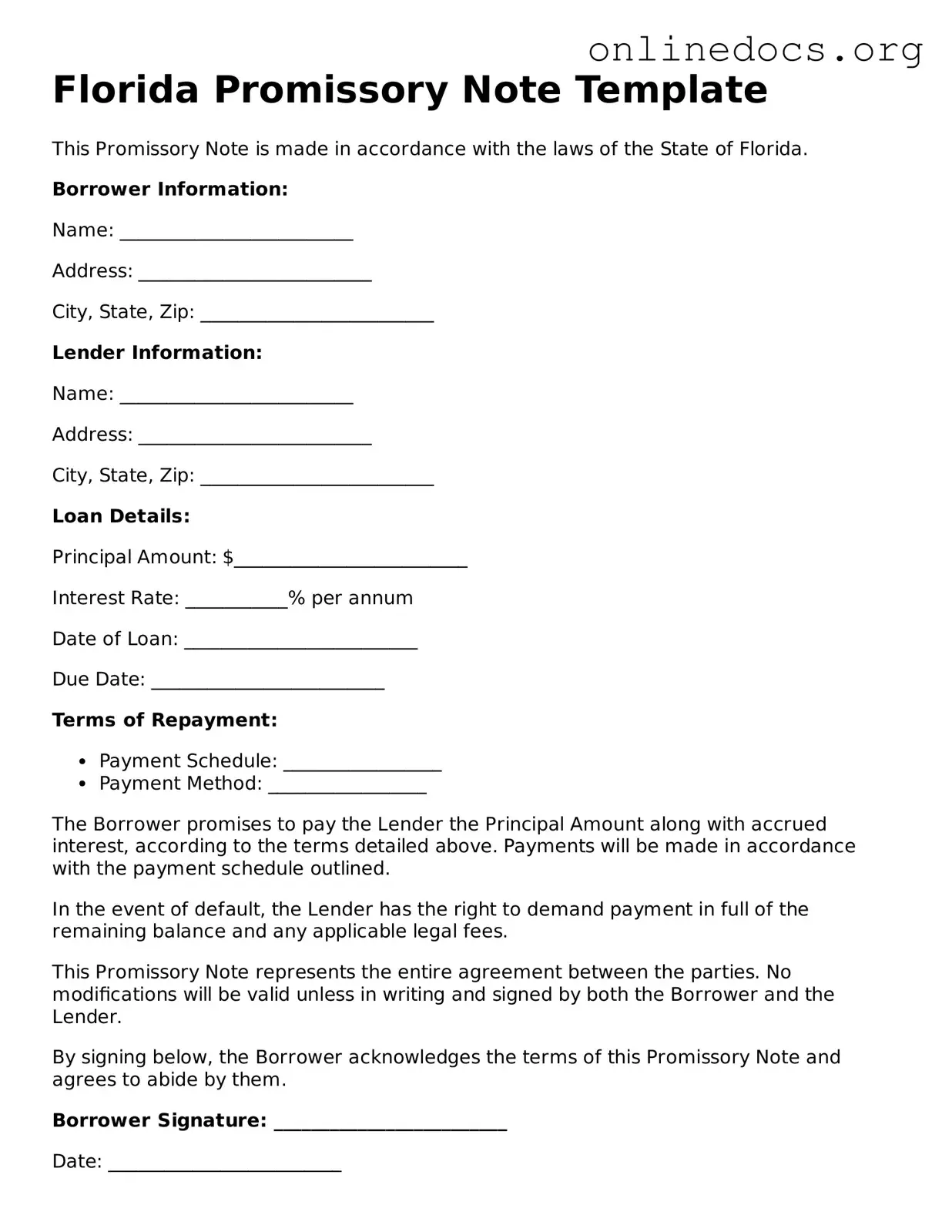

Completing a Florida Promissory Note form requires careful attention to detail. One common mistake is failing to include the correct names of the parties involved. It is essential that the borrower and lender's names are accurately spelled and reflect their legal identities. Any discrepancies can lead to confusion or disputes later on.

Another frequent error is neglecting to specify the loan amount clearly. This figure should be prominently stated, as it defines the total amount owed by the borrower. Omitting this detail or writing it incorrectly can create significant issues regarding repayment expectations.

People often overlook the importance of detailing the interest rate. The form must indicate whether the loan is interest-bearing and, if so, the exact rate. Without this information, both parties may have differing interpretations of the terms, which can lead to conflicts.

Additionally, many individuals fail to outline the repayment schedule. A clear timeline for payments, including due dates and the frequency of payments, should be established. Ambiguity in this area can result in misunderstandings regarding when payments are expected.

Another mistake is not including a provision for late fees. If the borrower fails to make a payment on time, having a specified late fee can incentivize timely payments. Omitting this clause may lead to financial losses for the lender.

Some individuals neglect to sign the document. A Promissory Note must be signed by both the borrower and the lender to be legally binding. Without signatures, the note lacks enforceability, rendering it ineffective in a legal context.

Inaccurate dates are another common issue. The date of execution should be included, as it marks the beginning of the loan agreement. Incorrect or missing dates can complicate the timeline of payments and obligations.

Furthermore, failing to provide a clear description of the loan purpose can create complications. Whether the funds are intended for personal use, business expenses, or another purpose, clarity in this area is beneficial for both parties.

Another oversight is not considering the inclusion of a default clause. This clause outlines the actions that will be taken if the borrower fails to meet their obligations. Without it, the lender may face challenges in enforcing their rights.

Lastly, individuals may not seek legal advice before finalizing the document. Consulting with a legal professional can help ensure that all necessary details are included and that the note complies with Florida law. This step can prevent potential issues and safeguard the interests of both parties.

Promissary Note Template - A Promissory note can help facilitate informal lending arrangements.

How to Write a Promissory Note for a Personal Loan - Borrowers may negotiate the terms before finalizing the note.

Additionally, to streamline the verification process and ensure compliance with state regulations, many employers opt to use resources from legalformspdf.com, which provides comprehensive templates and guidelines for properly completing the California Employment Verification form.

California Promissory Note Requirements - The document can include clauses for default remedies and legal fees.

Understanding the Florida Promissory Note form is crucial for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Below are five common misunderstandings about this important financial document.

While notarization can add an extra layer of security and authenticity, it is not a requirement for a promissory note to be legally binding in Florida. As long as the note includes essential elements like the amount borrowed, interest rate, and repayment terms, it can be enforceable.

Many people believe that promissory notes are reserved for significant amounts of money. In reality, these notes can be used for any sum, whether it's a small personal loan between friends or a larger financial transaction. The key is that both parties agree to the terms.

While verbal agreements can be legally binding, they often lead to misunderstandings and disputes. A written promissory note provides clear documentation of the terms, making it easier to enforce if necessary.

Not all promissory notes are created equal. The specifics of the note can vary widely based on the agreement between the lender and borrower. Different terms, interest rates, and repayment schedules can be tailored to fit individual circumstances.

While a signed promissory note is a binding agreement, it can be modified if both parties consent to the changes. It's essential to document any amendments in writing to avoid future disputes.

By dispelling these misconceptions, individuals can navigate the world of promissory notes with greater confidence and clarity.