Filling out the IRS 1120 form can be a daunting task, but adhering to some key guidelines can simplify the process. Here’s a list of essential dos and don’ts to keep in mind.

By following these guidelines, you can help ensure that your IRS 1120 form is filled out correctly and efficiently. Take the time to do it right; your business's financial health depends on it.

The IRS Form 1065 is similar to Form 1120 in that both are used by businesses to report their income and expenses to the Internal Revenue Service. However, while Form 1120 is specifically for corporations, Form 1065 is intended for partnerships. Partnerships do not pay income tax at the entity level; instead, the income passes through to the individual partners, who report it on their personal tax returns. Both forms require detailed financial information, including revenue, deductions, and credits, but they differ in how the tax liability is ultimately calculated and reported.

Another document that shares similarities with Form 1120 is the IRS Form 1040, which is the individual income tax return. While Form 1120 is used by corporations, Form 1040 is utilized by individuals to report their personal income, deductions, and tax liability. Both forms require taxpayers to detail their sources of income and applicable deductions, but the structure and reporting requirements differ significantly. Form 1040 focuses on personal income tax, while Form 1120 addresses corporate taxation.

Form 990 is also comparable to Form 1120, but it serves a different purpose. Nonprofit organizations use Form 990 to report their financial activities to the IRS. Like Form 1120, it requires detailed financial information, including revenue and expenses, but it is specifically designed for tax-exempt organizations. Both forms aim to provide transparency and accountability regarding financial operations, yet they cater to different types of entities and have distinct regulatory requirements.

When managing transactions, especially in real estate or vehicle sales, a crucial document to consider is the New York Bill of Sale. This form provides a comprehensive record of the transfer of ownership, detailing the seller, the buyer, and the specifics of the item being sold. For those seeking a reliable template or additional information, resources like legalformspdf.com can be invaluable in ensuring that all necessary legal aspects are properly addressed.

Lastly, Form 941, the Employer’s Quarterly Federal Tax Return, is related to Form 1120 in that both forms involve reporting to the IRS, but they serve different functions. Form 941 is used by employers to report payroll taxes withheld from employees’ paychecks and the employer’s share of Social Security and Medicare taxes. While Form 1120 focuses on corporate income and expenses, Form 941 is concerned with employment taxes. Both forms require accurate financial reporting and compliance with IRS regulations, but they apply to different aspects of taxation.

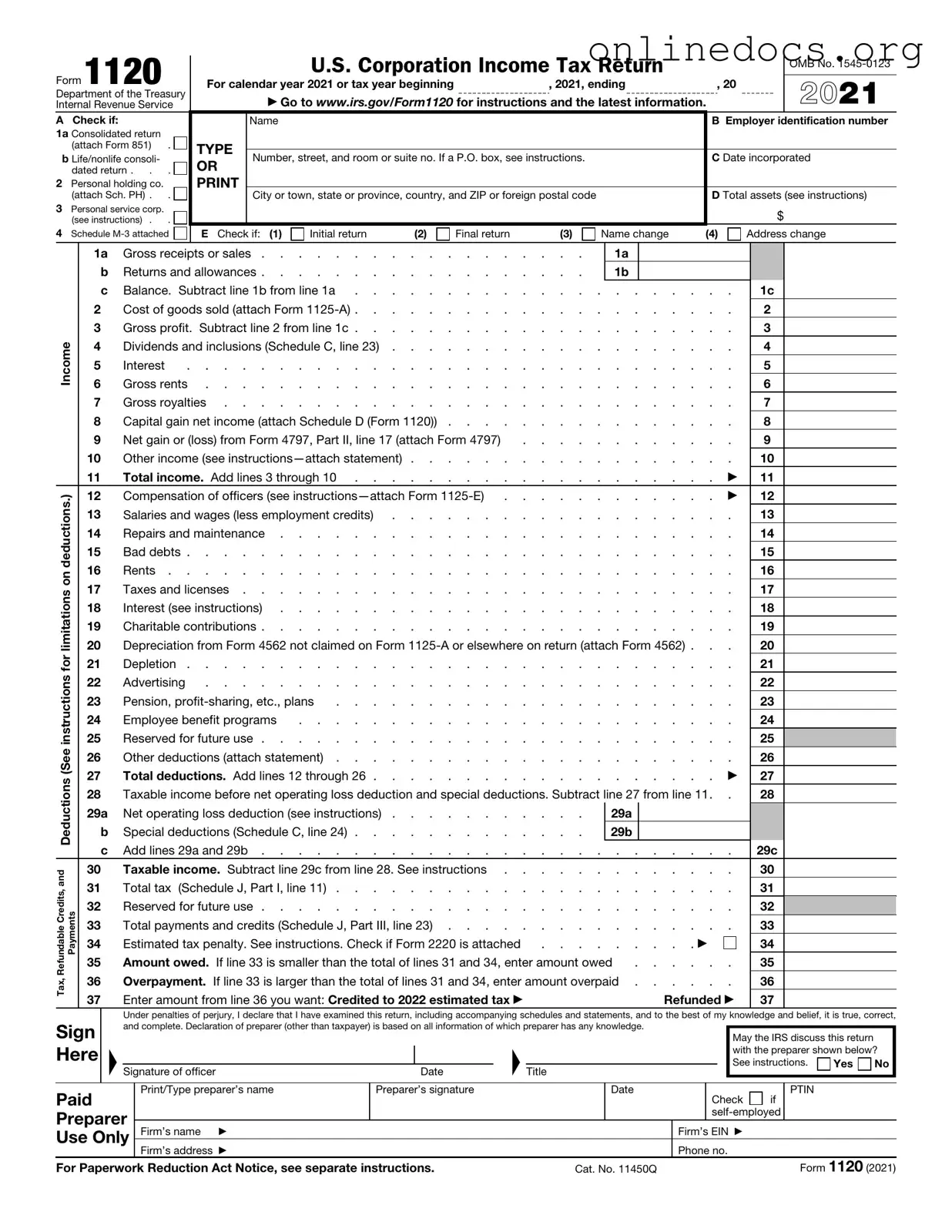

Filling out the IRS 1120 form can be a daunting task for many business owners. One common mistake is failing to report all income. Every dollar earned should be accounted for, including income from sales, services, and other sources. Omitting even a small amount can lead to penalties or audits.

Another frequent error is misclassifying expenses. It's essential to categorize expenses correctly to ensure compliance with tax laws. For instance, mixing personal and business expenses can create confusion and lead to incorrect deductions.

Many people also overlook the importance of signatures. The IRS requires the form to be signed by an authorized person. Neglecting to do so can result in the rejection of the return, causing delays and potential fines.

Inaccurate calculations are another common issue. Double-checking numbers is crucial. Simple math errors can change the amount owed or the refund expected, leading to unnecessary complications.

Some individuals forget to attach necessary schedules and forms. The IRS 1120 often requires additional documentation to support claims. Failing to include these can result in processing delays.

Not keeping proper records is a mistake that can haunt a business later. Maintaining organized financial records helps substantiate claims made on the form. Without proper documentation, it becomes challenging to defend against an audit.

Another pitfall is missing deadlines. The IRS has specific due dates for submitting the 1120 form. Late submissions can incur penalties and interest, which can add up quickly.

Some filers do not take advantage of available credits and deductions. Understanding what can be claimed is vital for minimizing tax liability. Ignoring potential savings means paying more than necessary.

Lastly, many people fail to seek help when needed. Tax laws can be complex, and consulting a professional can provide clarity. Ignoring this option can lead to costly mistakes.

By avoiding these common errors, business owners can ensure a smoother filing process and minimize the risk of complications with the IRS.

Roof Inspection Template - Identify the structure with a unique ID for easy reference.

Paperwork When Selling a Car - For sellers, providing their mailing address, too, is necessary.

For those looking to navigate the complexities of employment confirmation, our guide on the necessary steps for completing the Employment Verification form can be invaluable. By following the outlined procedures, you can ensure that your submission is both efficient and effective. For more information, visit our comprehensive Employment Verification form resource.

Salary Advance Format - Employees can alleviate financial stress by using the Employee Advance form.

The IRS Form 1120 is essential for corporations to report their income, gains, losses, deductions, and credits. However, several misconceptions surround this form. Below are eight common misunderstandings: