When filling out the Profit and Loss form, it's important to follow certain guidelines to ensure accuracy and clarity. Here’s a list of things you should and shouldn’t do:

The Profit and Loss (P&L) statement, also known as the income statement, shares similarities with the Balance Sheet. Both documents provide insights into a company's financial health, but they do so from different perspectives. The Balance Sheet presents a snapshot of a company's assets, liabilities, and equity at a specific point in time, while the P&L summarizes revenues and expenses over a period. Together, these documents help stakeholders assess profitability and financial stability.

The Cash Flow Statement is another document closely related to the Profit and Loss form. While the P&L focuses on revenues and expenses, the Cash Flow Statement tracks the inflow and outflow of cash within a business. It categorizes cash flows into operating, investing, and financing activities. By analyzing both documents, stakeholders can understand how operational performance translates into cash generation or consumption.

The Statement of Retained Earnings also shares a connection with the Profit and Loss statement. The P&L indicates net income or loss for a specific period, which directly impacts retained earnings. This statement outlines changes in retained earnings, including adjustments for dividends paid and the net income from the P&L. It provides a clearer picture of how profits are reinvested in the business or distributed to shareholders.

The Budget is another relevant document that complements the Profit and Loss form. While the P&L reflects actual financial performance, the Budget serves as a financial plan for future periods. It outlines projected revenues and expenses, allowing businesses to set targets and monitor performance against those goals. Comparing actual results from the P&L with the Budget can help identify variances and inform strategic decision-making.

In addition to financial documents, understanding leasing procedures is vital for both landlords and potential tenants. One essential resource in this process is the Rental Application form, which collects important details that help ensure a smooth rental experience for all parties involved.

Lastly, the Financial Forecast serves as a forward-looking counterpart to the Profit and Loss statement. While the P&L reports historical performance, the Financial Forecast estimates future revenues and expenses based on various assumptions. This document is crucial for strategic planning and can help businesses anticipate financial outcomes, manage resources effectively, and attract investors.

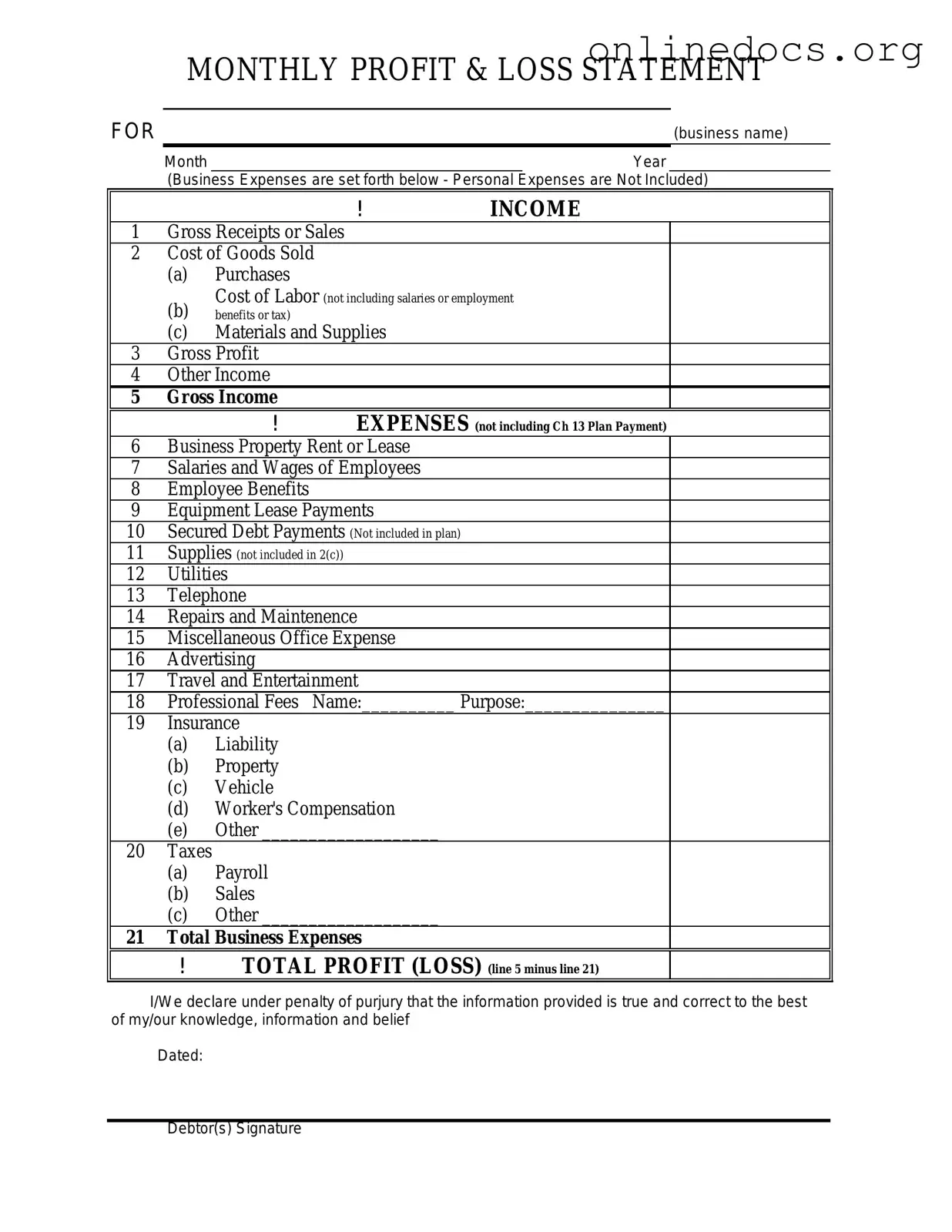

Filling out a Profit and Loss form is crucial for understanding the financial health of a business. However, many people make common mistakes that can lead to inaccurate reporting. One significant error is failing to keep accurate records of income and expenses. Without precise documentation, it becomes nearly impossible to provide a clear picture of profitability. Regularly updating records can help avoid this pitfall.

Another frequent mistake is mixing personal and business expenses. It's essential to keep these two categories separate. When personal expenses are included, it can distort the financial data and lead to incorrect conclusions about the business's performance. Maintaining distinct accounts for personal and business transactions simplifies this process.

Many individuals also overlook the importance of categorizing expenses correctly. Each expense should be assigned to the appropriate category, such as marketing, salaries, or utilities. Misclassification can lead to confusion and misinterpretation of where the money is going. Taking the time to categorize expenses accurately can provide valuable insights into spending habits.

Additionally, some people forget to account for all sources of income. It's easy to overlook secondary income streams, such as side projects or investments. Failing to report all income can result in an incomplete picture of profitability. Make it a habit to track all revenue sources to ensure comprehensive reporting.

Finally, many individuals neglect to review their Profit and Loss statement regularly. This document should not be a one-time effort; instead, it should be updated and analyzed periodically. Regular reviews allow for timely adjustments and better financial planning. By staying engaged with the Profit and Loss form, business owners can make informed decisions and drive their businesses forward.

Acord Binder - The Acord 50 WM is important for safeguarding employee rights in the workplace.

One essential resource for those looking to draft or understand a New York Residential Lease Agreement is found at legalformspdf.com, where you can access templates and detailed guidance to ensure a comprehensive understanding of the legalities involved. This ensures that both tenants and landlords have a clear framework for their rental relationship.

Paperwork When Selling a Car - Potential buyers should consult the Car Buyer’s Bill of Rights for more information.

Understanding the Profit and Loss (P&L) form is essential for anyone involved in managing finances, whether for a business or personal use. However, several misconceptions can lead to confusion. Here are nine common misconceptions about the P&L form, along with clarifications for each:

Individuals managing personal finances or freelancers tracking income and expenses can also benefit from a P&L form.

In reality, it details both income and expenses, providing a complete picture of financial performance.

While they are useful during tax season, these forms also help in budgeting and financial planning throughout the year.

Not every expense listed on a P&L form can be deducted for tax purposes. Understanding which expenses qualify is crucial.

Profit on a P&L form reflects earnings, but it doesn’t always equate to actual cash available. Timing differences can affect cash flow.

It is a dynamic document that should be updated regularly to reflect current financial conditions and performance.

While accountants have expertise, anyone with a basic understanding of finances can create and maintain a P&L form.

They serve different purposes. The P&L form shows performance over a specific period, while a balance sheet reflects assets and liabilities at a specific point in time.

Even small businesses can benefit from tracking income and expenses to make informed decisions and monitor growth.

By addressing these misconceptions, individuals and businesses can gain a clearer understanding of their financial health and make better-informed decisions.