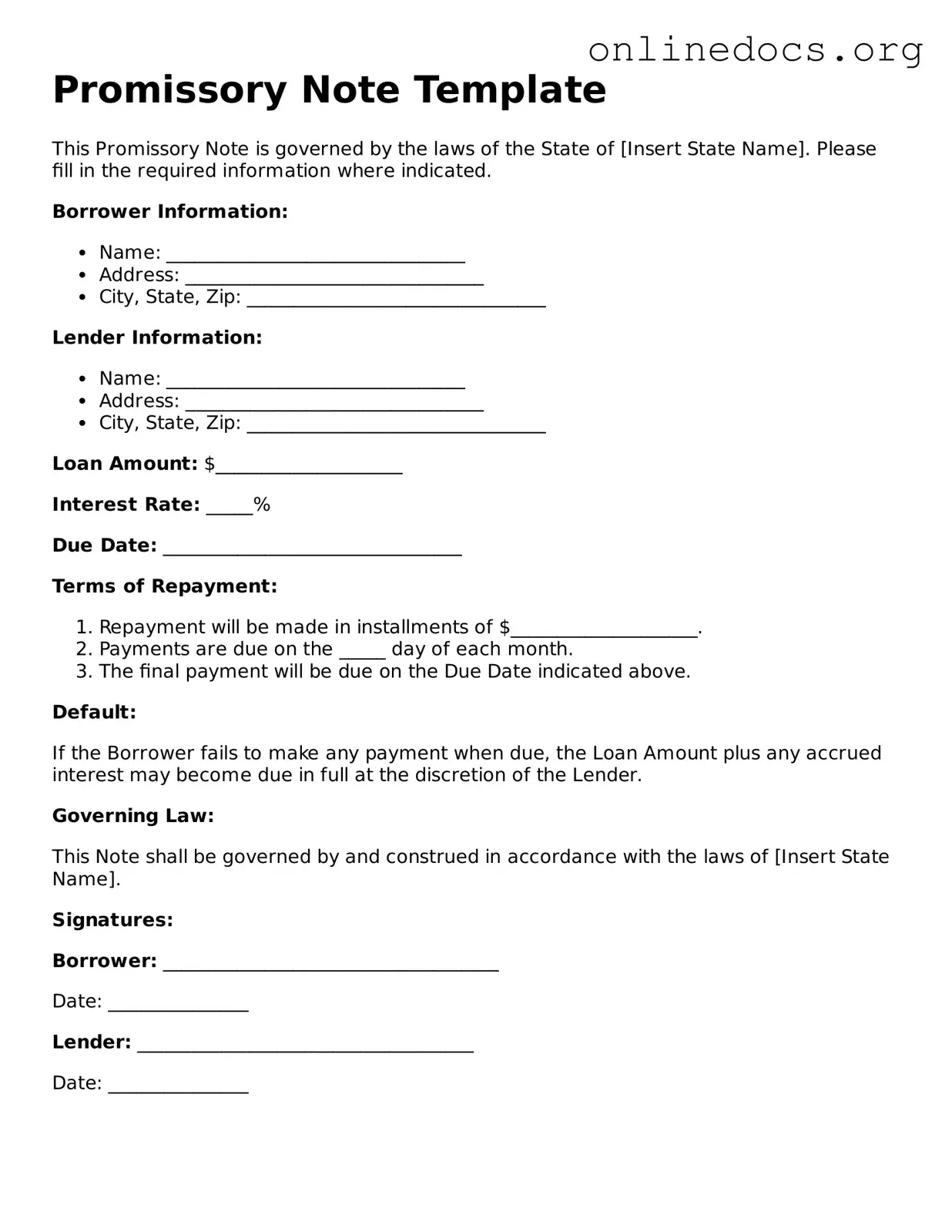

When filling out a Promissory Note form, it’s important to be thorough and accurate. Below is a list of things you should and shouldn't do to ensure your document is completed correctly.

A loan agreement is a document that outlines the terms of a loan between a borrower and a lender. Like a promissory note, it specifies the amount borrowed, the interest rate, and the repayment schedule. However, a loan agreement often includes additional details such as collateral requirements and the consequences of default. This document provides a more comprehensive framework for the lending relationship, ensuring both parties understand their rights and obligations.

A mortgage is another document similar to a promissory note, but it specifically pertains to real estate transactions. In a mortgage, the borrower agrees to repay the loan used to purchase property, while the lender holds a lien on the property as security. While a promissory note focuses on the borrower's promise to pay, a mortgage emphasizes the legal claim the lender has on the property in case of default.

To ensure clarity and understanding among employees regarding workplace expectations, having an Employee Handbook is essential; it not only provides guidance on company policies but also emphasizes the significance of all employment-related documents. For those looking to create or refine such resources, legalformspdf.com offers a wealth of information that can help in drafting a comprehensive handbook tailored to specific company needs.

A personal guarantee is a document where an individual agrees to be responsible for the debt of a business or another person. Similar to a promissory note, it serves as a commitment to repay a debt. However, it differs in that it often involves a third party who is not the primary borrower. This document provides additional security for lenders, as it holds the guarantor personally liable if the primary borrower fails to fulfill their obligations.

An IOU, or "I owe you," is a simple acknowledgment of a debt. It is less formal than a promissory note and may not include detailed terms like interest rates or repayment schedules. While both documents signify a debt, an IOU is often used for smaller, informal loans between friends or family. Its simplicity makes it accessible, but it lacks the legal enforceability typically found in a promissory note.

A lease agreement shares similarities with a promissory note in that it outlines a payment obligation. In a lease, a tenant agrees to pay rent to a landlord for the use of property over a specified period. While a promissory note focuses on a loan repayment, a lease agreement emphasizes the rental terms and conditions. Both documents serve to protect the interests of the parties involved by clearly stating the expectations regarding payments.

A credit agreement is another relevant document that defines the terms of borrowing. It is often used by businesses to secure lines of credit. Like a promissory note, it details the amount borrowed and repayment terms. However, credit agreements can be more complex, including provisions for fees, covenants, and other conditions that govern the borrowing relationship. This document provides a broader context for the financial arrangement, often involving multiple transactions over time.

A bond is a formal contract to repay borrowed money at a fixed interest rate over a specified period. Similar to a promissory note, a bond represents a promise to pay. However, bonds are typically issued by corporations or governments and can be sold to investors. This makes them distinct from promissory notes, which are usually personal agreements. Bonds often come with additional features, such as callable options or conversion rights, adding layers of complexity to the agreement.

Filling out a Promissory Note can seem straightforward, but many people stumble along the way. One common mistake is not clearly stating the loan amount. This figure should be precise, and any ambiguity can lead to confusion down the line. If the amount is written incorrectly, it can result in disputes. Always double-check the numbers!

Another frequent error involves the interest rate. Some individuals either forget to include it or miscalculate it. This can create misunderstandings about how much the borrower will ultimately owe. It’s crucial to specify whether the interest is fixed or variable and to ensure that the rate is compliant with state laws.

People often overlook the importance of identifying all parties involved. Not including the full legal names of both the borrower and lender can lead to complications. If a dispute arises, proving who is involved becomes much harder. Make sure to include accurate contact information for both parties to avoid any issues.

Additionally, many forget to include a clear repayment schedule. This means specifying when payments are due and how they should be made. Without this information, the borrower may not know when to pay or how much to pay, leading to potential late fees or misunderstandings.

Another common mistake is failing to sign and date the document properly. A Promissory Note is not legally binding until it is signed by both parties. Neglecting to do this can render the entire agreement void. Always ensure that signatures are present and that the date is clearly marked.

Lastly, people sometimes neglect to consider what happens in case of default. Including a clause that outlines the consequences of failing to repay the loan is essential. This can protect both the lender and borrower by providing a clear understanding of the next steps if payments are missed.

CBP Form 6059B - Submitting a completed CBP 6059B ensures a smoother customs process.

For those looking to manage their financial or healthcare decisions effectively, a vital tool is the important Power of Attorney document. This form not only designates someone to act on your behalf but also ensures that your preferences are respected during critical times.

Puppy Bill of Sale Template - Provides guidelines for proper dog care post-purchase.

Salon Contract Template - Allows both parties to specify any unique terms or conditions for the rental.

Understanding the Promissory Note form can be challenging, and several misconceptions often arise. Here are six common misunderstandings that people may have:

All Promissory Notes Are the Same. Many believe that all promissory notes are interchangeable and follow a one-size-fits-all template. In reality, the terms and conditions can vary significantly based on the agreement between the parties involved, the amount of money, and the repayment schedule.

Promissory Notes Are Only for Loans. Some people think that promissory notes are only used for formal loans. However, they can also be used in various situations, such as personal loans between friends or family members, and even in business transactions.

A Verbal Agreement Is Enough. There is a misconception that a verbal agreement suffices for a promissory note. While verbal agreements can be binding, having a written promissory note provides clear documentation and can prevent misunderstandings or disputes down the line.

Only Financial Institutions Use Promissory Notes. Many people assume that only banks and financial institutions utilize promissory notes. In truth, individuals and businesses of all sizes can and do use them to formalize lending agreements.

Signing a Promissory Note Guarantees Payment. Some believe that merely signing a promissory note guarantees repayment. While it serves as a formal acknowledgment of the debt, it does not eliminate the risk of default. The ability to collect on the note often depends on the borrower's financial situation.

Promissory Notes Cannot Be Transferred. A common myth is that once a promissory note is signed, it cannot be transferred to another party. In fact, many promissory notes are negotiable instruments, meaning they can be sold or transferred to others, subject to certain legal requirements.

By addressing these misconceptions, individuals can better understand the role and importance of promissory notes in financial agreements.